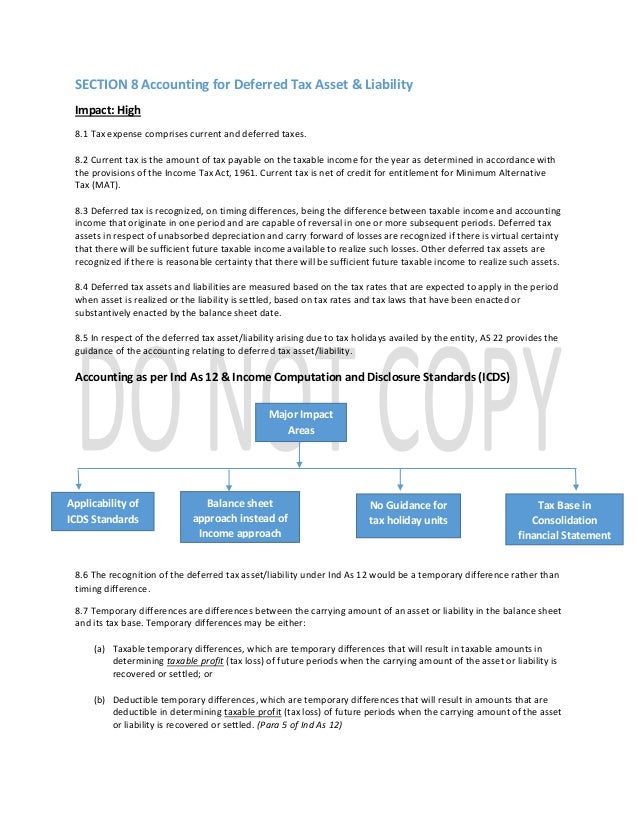

Mat Credit Entitlement Ind As

Guide To Minimum Alternate Tax For Ind As Compliant Companies

Http Www Bancoindia Com Wp Content Uploads 2018 05 Afrbpil2018 Pdf

Standalone Financial Statements Mindtree

Mat Credit Whether Credit For Surcharge And Education Cess On Brought Forward Mat Credit Is Available The Tax Talk

Http Www Cpil In Downloads 2018 19 Financial Results March 2018 Pdf

Impact Of Ind As On E Commerce

The asset may be reflected as mat credit entitlement.

Mat credit entitlement ind as.

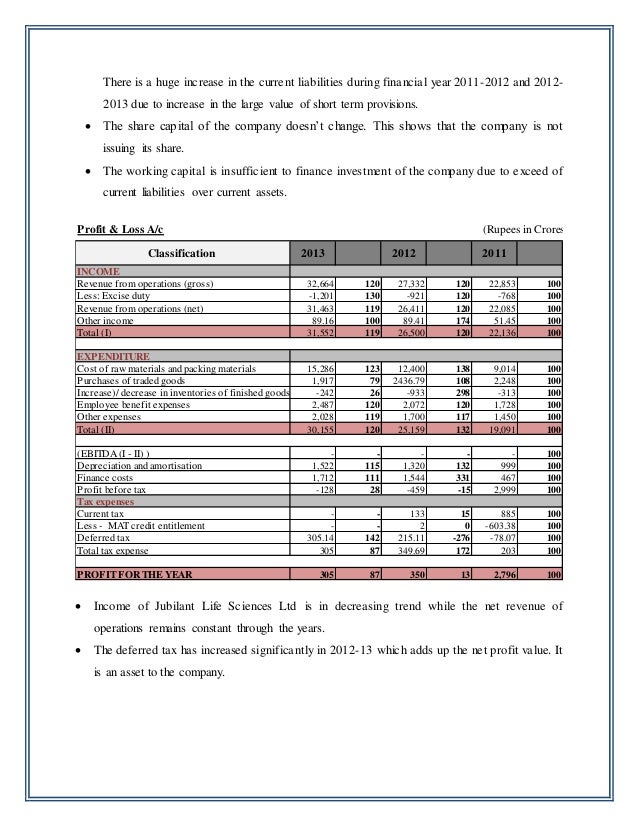

Common Size Trend Analysis Of Financial St Of Pharma Co

Significant Accounting Policies And Notes To The Accounts For The Year Ended March 31 2013 Mindtree

Http Www Nagpurpowerind Com Wp Content Uploads 2019 08 Audit 20report 20fy 202018 19 Pdf

Http Maxvil Com Wp Content Uploads 2017 11 Maxvil Q2 Fy 2018 Financial Results Stand Alone Pdf

Consolidated Financial Statements Mindtree

Consolidated Financial Statements Mindtree

Https Www Dishmangroup Com Files Dishmangroup Investor Relations Carbogen 20amcis 20 India 20ltd Pdf

Sutlej Textiles Industries Fundamental Analysis Dr Vijay Malik

Https Www Indiabullsintegratedservices Com Subsidiary Companies Sentia 20properties 20limited Pdf

Https Icvl In Pdf Icvl 1 Standalone I Pdf

Https Www Pwc In Assets Pdfs Publications 2018 Ind As Presentation And Disclosure Checklist 2018 Pdf

Http Taalent Co In Pdf Tel Results 31 March 2019 Pdf

Http Www Jalindia Com Annualreports Annualreportsofsubsidiarycompanies 2017 12 Jaypee Cement Corporation Limited Pdf

Http Www Texinfra In Pdf Startree Signed 16 17 Pdf

Http Www Jalindia Com Annualreports Annualreportsofsubsidiarycompanies 2017 15 Yamuna Expressway Tolling Limited Pdf

Https Www Havells Com Havellsproductimages Havellsindia Content Pdf About Havells Investor Relations Financials Quaterly Results 2018 2019 Quaterly Results4 Published Resultsq4andfy19 Pdf

Https Shipindia Com Upload Financialresult Results Q1 19 201 Pdf

Https Www1 Nseindia Com Corporate Bls 16072020143657 Replytoclarificationscan Pdf

Http Www Gammonindia Com Investors Pdfs Fy16 17 Atsl 20infra Pdf

Https Www Aarti Industries Com Media Investors Subsidiary 1536579693 Innovative Envirocare Jhagadia Limited Balance Sheet As Nagnzjt Pdf

Consolidated Financial Statements Pdf Free Download

Http Www Bseindia Com Bseplus Annualreport 533189 5331890318 Pdf

Https Www Tatapowerrenewables Com Pdf Statement 31mar2018 Pdf

Http Www Nagpurpowerind Com Wp Content Uploads 2018 09 Mmcpl Balancesheet17 18 Pdf

Source : pinterest.com